Beppe Grillo’s Five Star Movement riding high in the polls in Italy has led to speculation over the prospect of the country leaving the euro. Lorenzo Codogno and Giampaolo Galli argue that an “Italexit” would be a catastrophic scenario, with incommensurable economic, social, and political costs lasting for many years. They note that redenomination, and a likely default on debt obligations, would not be a solution to the problem of a high public debt and would produce significant financial and economic instability. A far better and less costly solution would be to address Italy’s underlying problems, allowing the country to survive and thrive within the euro by enhancing potential growth and economic resilience.

In recent times, there has been a rising populist mood in Europe against the European Union (EU), the European Economic and Monetary Union (EMU), and the euro. Italy is no exception. Brexit and the rise of anti-establishment movements have bolstered this trend across the continent. Exit from the EU is doable, although hugely disruptive and complex, as the United Kingdom is now discovering the hard way. However, exit from the monetary union would be disruptive on a very different scale and could negatively affect the involved country’s economy for a number of years. Moreover, it may simply not solve the problems some people claim it would solve. Putting aside political motivations, some commentators, such as the authors of a recent Mediobanca Securities paper,1 have argued that leaving the euro is doable and that there are costs and benefits that need to be considered. They concluded that Italy would even reap a small benefit (8 billion euros) by getting out and also provided technical arguments on the effects of debt redenomination, arguing that redenomination in the future would be too costly and thus, the sooner the better. We strongly disagree.

First, the economic argument. The European Economic and Monetary Union is a huge project that has revealed numerous fragilities and problems during the financial crisis. Many of these problems are still wide open. Italy’s economy has performed badly since the launch of the euro and even in the convergence process that preceded monetary union. This is undeniable. Still, it is far less clear if this has much to do with monetary union itself or the strength of the euro. Many global phenomena occurred almost at the same time, starting from China’s entry into the World Trade Organisation, the surge of global supply chains, deep technological changes in communication, logistics, and many other sectors, as well as profound changes in the organisation of labour, with machines replacing workers and the “Uberisation” of services. All these phenomena have very little to do with the euro. In fact, it can be argued that Italy missed the opportunities offered by the Single Market and European integration. Hence, the underlying problems may well be unrelated to the euro and have more to do with Italy’s inability to adapt to the structural changes in the global economy. Therefore, if the euro was not the problem, Italexit would not be the solution.

Political Will vs. Economic Logic

Italexit may happen for three reasons: (1) political will overcoming economic logic; (2) continuing poor economic performance, with those unable to remain competitive calling for devaluation and departure from the single currency, combined with the inability to curb public deficits resulting in unsustainable public debt-to-GDP dynamics; and (3) financial market participants spotting the above two factors and producing a self-fulfilling prophecy. The second argument is weak, in our view, as would probably create more damage than benefits, and it would thus be much better to address the underlying problems instead. The latter argument is clearly a danger – if the perceived risk of (1) and (2) rises and pushes Italy’s government bond spreads up, Italexit would indeed become a self-fulfilling prophecy.

Political will may certainly counter economic logic, especially if we take some of the Five Star Movement’s statements at face value. Here is one example:2

“The Euro is the heist of the century: it is not irrevocable, as Mario Draghi decided. Break the cage; regain the sovereignty sold off to kleptocrats, technocrats, and oligarchs. Rebuild from the rubble the Europe of people, calling upon citizens to express themselves with a referendum.”

Other statements openly suggest3 that Italexit would go hand in hand with a default on debt obligations. If these statements are taken seriously and the perceived risk of the Five Star Movement taking power increases, then what is now an extremely low probability event may turn into a self-fulfilling prophecy, even before any political shift actually happens. Moreover, in the next section, we argue that the suggested arithmetic of redenomination is misleading and self-defeating. We will then turn to the more general theme of exit from a monetary union.

Redenomination is Not a Solution

We start with the redenomination theme because it has recently attracted attention even among rather sophisticated economists and policy makers (e.g. Mediobanca Securities paper).

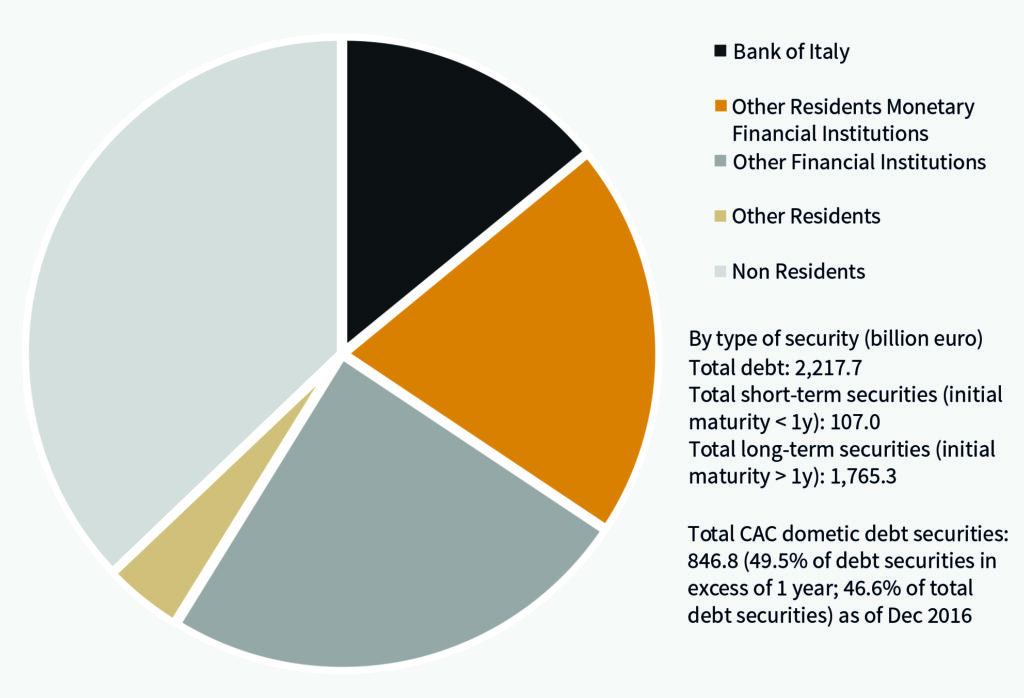

Their argument goes as follows. In the case of an exit, the Italian government could not redenominate the bonds issued after 1 January 2013 with initial maturities exceeding one year because such bonds are subject to the Collective Action Clause (CAC). According to our estimates, at the end of 2016, there were 847 billion euros in outstanding domestic bonds subject to CAC, equivalent to 49.5% of outstanding debt securities in excess of one year or 46.6% of total debt securities (see Figure 1 on next page). According to the authors of the Mediobanca Securities paper, Italy could still redenominate the bonds issued before 1 January 2013. Following exit and a 30% devaluation, the government would lose 280 billion euros on the portion of debt that cannot be redenominated (including bonds issued under foreign law and derivatives) and would “gain” 191 billion euros on the portion of debt that would be redenominated.

The authors made three wrong assumptions:

(1) The mere existence of CAC de iure does not prevent a sovereign state from redenominating its debt (although redenomination triggers CAC). What matters the most is the legislation under which the securities were issued, i.e. Italian legislation for all domestic securities. As a result, at least in theory, all domestic obligations could be redenominated. Also, please note that, if there is no redenomination, the debt-to-GDP ratio would go to 190% under the assumption of a 30% devaluation, making default very likely.

(2) Moreover, derivatives are all under national legislation and can thus be redenominated.

(3) Finally, of the debt denominated in other currencies, which amounts to about 48 billion euros, only 9 billion falls under foreign legislation (USD bonds under New York legislation and a few EMTN under German legislation, i.e. Shuldschein). This also implies the possibility of redenomination.

Under the further – and indeed, quite bold – assumption that EU partners agree to inflate the QE bonds away, the authors conclude that Italexit would imply a gain of 8 billion euros. This is, of course, a very small sum, but this is not the point. The point is that this whole exercise conveys the impression that (a) the fear of an increase in the already very large burden of Italian debt following an exit is misplaced, and, more importantly, (b) the cost-benefit analysis for leaving the euro can be confined to direct short-term financial costs or benefits for the Treasury.

The former is clearly flawed reasoning because the redenomination of non-CAC government bonds produces no financial gain whatsoever for the government. It simply eliminates the loss incurred on the bonds that are not redenominated when exit from monetary union occurs. The elimination of loss is, of course, very different from the emergence of gain. On the liabilities side of the government balance sheet, expressed in the new domestic currency, there would be a loss on the portion of debt not redenominated and no change on the portion that is redenominated. Hence, the redenomination would cap the loss, but it would certainly not lead to gain.

In order to reap the gains that the authors claim would stem from redenomination, the government would effectively have to partly or entirely renege on the debt, and, following redenomination, some form of default would indeed look very likely. In that case, the liabilities side of the government balance sheet would record a loss on the portion of debt that is neither redenominated nor reneged and a gain on the portion that is reneged.

It is also important to recall that not adhering to the contractual obligations to its creditors, including payment in the currency stipulated, would trigger4 a declaration of default by rating agencies. Needless to say, whatever problems one can see with redenominating the debt (in terms of reputation, future access to markets, etc.) would be compounded by a deliberate debt write-off on top of redenomination.

L’articolo originale può essere letto qui.